Impact Fee Update and 2015 Outlook

June 25, 2015 | Energy

This research brief analyzes calendar year (CY) 2014 impact fee revenues (remitted April 2015) reported by the Pennsylvania Public Utility Commission (PUC) and potential scenarios for CY 2015. The research brief also translates the impact fee into an annual average effective tax rate (ETR) based on natural gas price and production data. The ETR is a metric that quantifies the implicit tax burden imposed by the impact fee in a given year.

The annual impact fee for an unconventional natural gas well is determined according to a bracketed schedule based on the number of years since a well became subject to the impact fee (operating year), the type of well (horizontal or vertical) and, to a limited extent, the annual average price of natural gas.

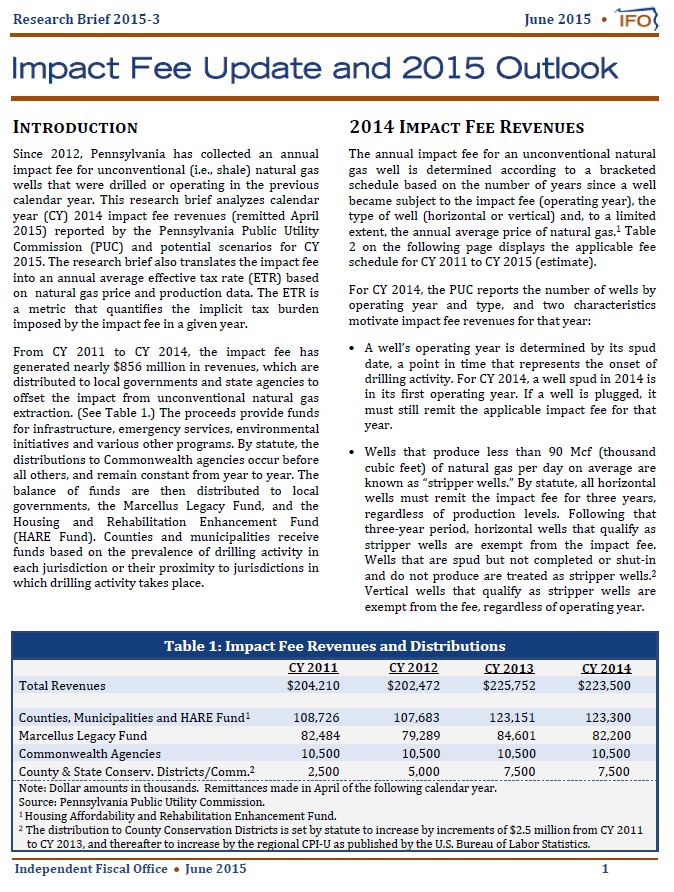

For CY 2014, impact fee revenues total $223.5 million, which is based on the published fee schedule and well counts. Those revenues differ from previous years in two respects. First, CY 2014 was the first year that the number of unconventional wells spud in Pennsylvania exceeded the number spud in the prior year. Due to that outcome, the statute requires the PUC to apply a regional inflation adjustment to the fee schedule. The inflation adjustment increased collections by an estimated $1.2 million. Second, CY 2014 was the first year in which horizontal stripper wells were eligible for an exemption after paying the fee for three years (i.e., in their fourth operating year). The horizontal stripper well exemption reduced collections by an estimated $7.4 million. For CY 2015, a baseline scenario suggests that 1,067 new wells and 6,893 existing wells could be subject to the impact fee. The final section of this research brief provides additional detail regarding that and other potential scenarios.